The bond bubble is cracking, and societies are breaking apart. From Moneyweb.

The trillions rammed into the ‘economy’ benefitted the few while while millions lost their jobs and homes. Image: Shutterstock

The financial markets have their share of gloom merchants who are always predicting financial collapse. Once every decade or so, they turn out to be correct, but listening to them you risk missing out on some spectacular market gains.

But what when sober and pragmatic fund managers such as Donald Amstad from Aberdeen Standard Investments, with £583 billion under management in 80 countries, warn of imminent collapse in the West?

In particular, he is warning of a collapse in the one asset class traditionally regarded as a safe haven – bonds. The West has reached the end of the road as far as quantitative easing (QE) is concerned. As interest rates drop to zero or lower, central banks will be tempted to fire up the printing presses yet again, but this time banks, pension funds and insurance companies will go bust.

Read: SA won’t consider quantitative easing to help Eskom – Masondo

Amstad used some alarming language in an interview he gave with Livewiremarkets.com, warning of social collapse and even civil war in countries such as the US. Fund managers typically have a commercial bias towards rising asset prices.

Read: These three factors will shape the investment climate of 2019 – JP Morgan

Those who have lived through a few market crashes will recall the admonition of these managers to remain faithful, trust the markets, and wait for the rebound. And they’ve generally been correct. Up to now.

Massive money printing in the post-2008 financial era has not been particularly inflationary for consumers.

This has given rise to the mistaken notion that money printing can be carried on forever without consequence. But there are consequences.

Those billions and trillions of currency rammed into the ‘economy’ have ended up inflating stock and bond prices, to the ultimate benefit of the 1% of the 1%, while millions of ordinary people lost their jobs, their houses and their livelihoods.

In economic terms, this is called the Cantillon effect, named after 18th Century economist Richard Cantillon, who observed that new money created does not filter through the economy evenly. The first to benefit are those sitting closest to the money, such as banks and big companies. They get to take this new money onto their balance sheets first, spend it, and only later does inflation start creeping into the rest of the economy.

It’s a form of redistribution from the poor to the rich. This is precisely what has happened since 2008.

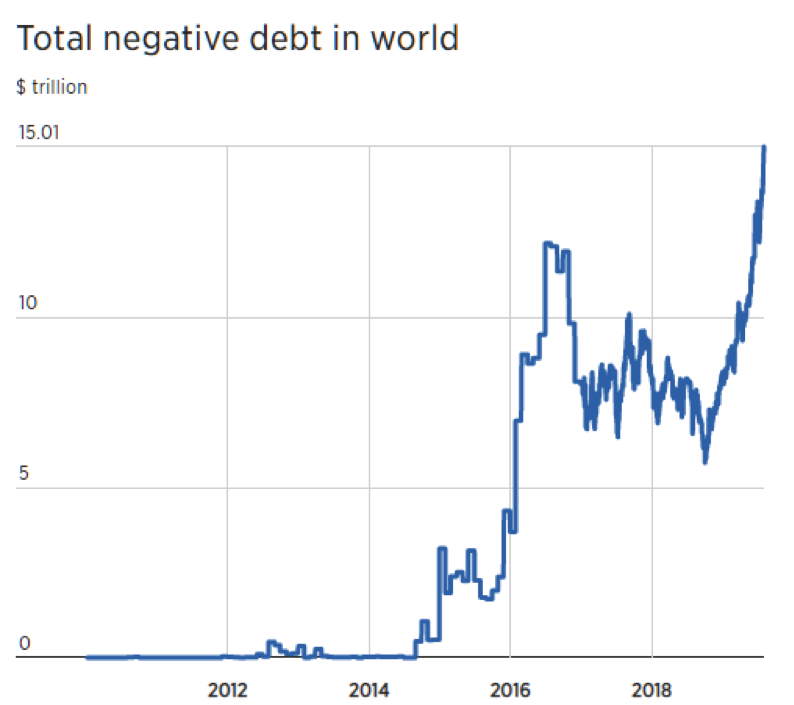

What has alarmed Amstad, among others, is the fact that so much toilet paper money is floating around the global economy that yields have turned negative.

This means you are losing money by investing in bonds in Japan, Switzerland and elsewhere. Put another way, investors are paying governments to keep their money safe. The following chart from Deutsche Bank shows how much global debt is being invested at negative interest rates.

Source: Deutsche Bank

During the emerging market crisis of the 1990s, every country wanted to print money to arrest the crunch. The International Monetary Fund (IMF) stepped in and dissuaded them from doing that, warning that they risked becoming basket cases like Zimbabwe. Asian central banks and governments heeded the IMF’s advice: companies and banks went bust and unemployment shot up, but eventually the green shoots started to appear and Asia emerged from the crisis within a few years.

The calamities that followed

Nearly a decade later it was the tech bubble that burst. Investors were persuaded to abandon common sense and invest huge amounts of money in companies that had yet to turn a profit.

In 2007 and 2008 it was the sub-prime mortgage crisis. Western banks warned unless they were bailed out, financial Armageddon was at hand. Central banks surrendered and started a massive campaign of quantitative easing. All that did was keep equity and bond prices aloft. As US economist Michael Hudson has pointed out, it would have been far better if this money was thrown from helicopters to ordinary people in financial distress. Instead, it was used to fatten the balance sheets of the big banks and enrich their executives.

Printing money, cutting rates

When the 2008 crisis hit in the West, the IMF’s ministrations involved printing money and cutting rates as if the planet’s very survival depended on it. It was advising Western governments to do the exact opposite of what it was advising Asian governments in the 1990s.

Amstad says we are now in the extraordinary situation where 10-year Swiss government bonds are yielding nearly -1%, and even 50-year bond yields have turned negative. Thirty-year US Treasury bonds are now yielding less than 2%, and US President Donald Trump wants to see interest rates lower still.

“These are dangerous times,” says Amstad. “The difference between [the] emerging and the developed world is that the West is on a cliff edge and is running an unorthodox monetary policy.”

Emerging countries have less debt, fewer liabilities and more orthodox money policies. Though they will suffer from any global financial contraction, they will rebound quicker.

Ironically, emerging markets now appear as a safe haven. It is the developed world that is at risk.

A negative yield curve is usually a harbinger of recession, but this time Western central banks have very little firepower left to refloat their economies. Should the world enter recession at a time when no one is earning interest on their savings, corporate and banking failures are inevitable.

Banks make money when interest rates are high, yield curves are steep (in other words, interest earned on longer-term bonds are significantly higher than on shorter-term bonds), and credit spreads are wide. We now have the opposite of these three conditions in most of the developed world, but especially in Europe. Banks struggle to make money when yield curves are negative. The recent spike in market volatility is a sign of growing panic, and funds are rushing into cash – which at least holds its value in nominal terms.

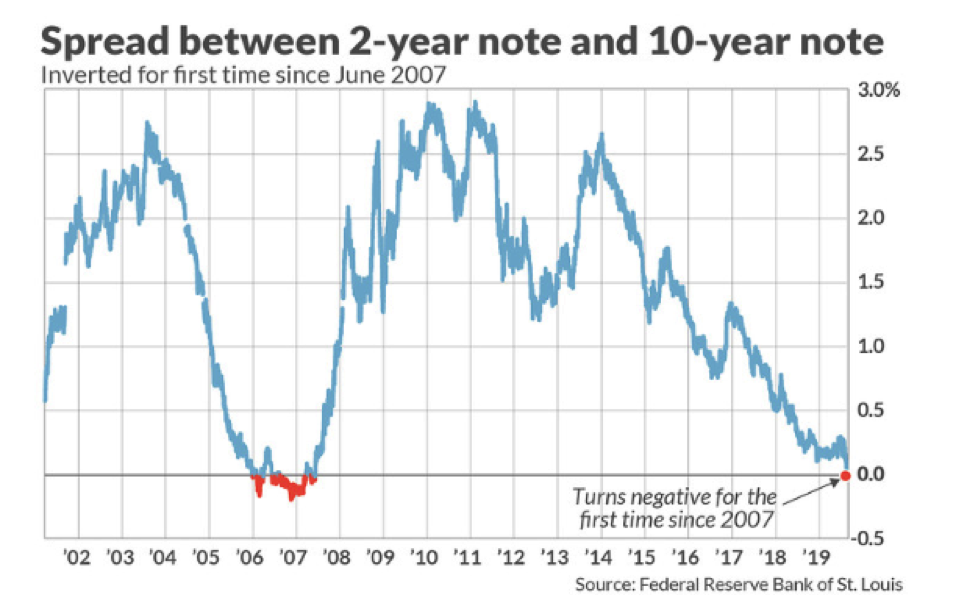

Not only are bonds paying next to nothing in interest, but their yield curves have also turned negative – meaning longer-term bonds are paying out less than shorter-term bonds.

Investors expect to receive a higher rate of interest for investing for a longer period of time. When shorter-term bonds pay out more than longer-term bonds, a recession is usually not far behind.

Source: Federal Reserve Bank of St Louis, US

The problem is aggravated when pension funds are factored into the equation. US government debt currently stands at $21 trillion, yet its liabilities are probably 10 times this amount – about $124 trillion. Says Amstad: “To the man in the street this means [the] US government has promised to pay this amount but has not funded it. Where the hell is the US government going to get $124 trillion from? It just cannot be done.”

The result will be a fight over who gets whatever the US government is able to pay, which is where it gets frightening. Civil war may be the result. If you are gay, Muslim, black or a woman, you are already under attack, says Amstad. The UK government is in similar straits. Italy is threatening to leave the European Union, and the UK is in a political crisis over Brexit. Society is breaking down.

“What we have never had to cope with before is if there is a bubble in the risk-free asset class. What happens when that goes pop. What is the new risk-free?”

China is on a different path. It is solvent, has low levels of debt, low levels of liability, and an asset-packed balance sheet with state-owned enterprises that are massively profitable.

The West is going to have to own up to a failed economic experiment and take its medicine.

That means allowing any recession to play out, and with that expect to see some spectacular corporate and banking failures.